Sukanya Samriddhi Yojana (SSY)

The Sukanya Samriddhi Yojana is a girl child prosperity scheme under the “Beti Bachao Beti Padhao” program of Prime Minister Narendra Modi.

It is a government-backed savings scheme designed for the benefit of the girl child. The main purpose of this investment scheme is to ensure a bright future for girl children in India by facilitating them with proper education and care-free marriage expenses. This scheme allows the parents/guardian of the girl child to open a savings deposit with the designated financial institution. The money deposit in the account earns tax-free interest which is compounded annually. The current interest rate is 7.6%.

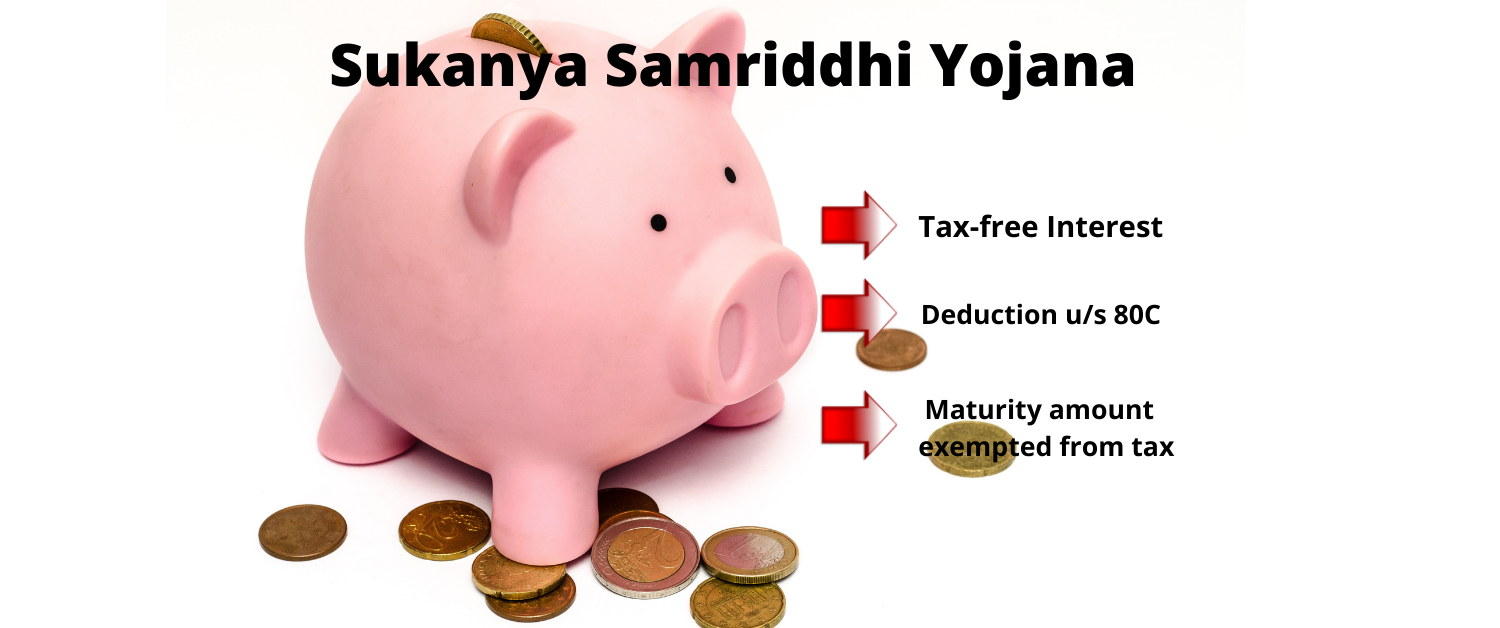

The biggest advantage of opening an SSY account is that it falls under the EEE exemption scheme which means that:

- The interest earned under this scheme is completely tax-free.

- The amount received on maturity is exempted from tax.

- The amount invested is eligible for claiming deduction u/s 80C.

The government has authorized various financial institutions for the opening of accounts under this scheme. One can open an SSY account with any of the authorized Banks or Post Office. You can also set it up online with the help of a net banking facility. Money can be deposited in the account by way of Cash/Cheque/ Demand Draft/transfer through Internet Banking. Standing Instructions can also be given at the Branch for automatic credit to Sukanya Samriddhi Account.

Key Highlights of the Scheme:

| Who can open this account? | A natural/legal guardian of a resident girl child can open this account on her behalf. This means that the account can also be opened for an adopted girl child. |

| Minimum Investment Amount

Maximum Investment Amount |

Rs. 250/-

Rs. 1,50,000/- |

| Current Interest rate | 7.6%

The interest is compounded annually and shall be credited to the account at the end of each financial year. Interest shall be calculated for the calendar month on the lowest balance in the account between the close of the 5th day and the end of the month. Hence, if you plan to invest in the SSY scheme, it’s best to do it before the 5th of the particular month to receive the benefit of interest income for that month. |

| Tax benefit | EEE benefits–

Interest : Tax-free Maturity Amount : Tax-free The amount deposited is eligible for deduction u/s 80C |

| Lock-in period | 5 years with conditional withdrawal after 5 years*. |

| Time before which account can be opened | Account should be opened before the girl child attains the age of 10 years. |

| No of years for which deposit can be made | 15 years, including the years in which the account is opened. After 15 years deposit is optional for up to 21 years. |

| Can the account be operated online? | Yes |

| Is the account transferable to any part of the country? | Yes |

| Can a person avail a loan under this scheme? | No |

| Maturity | The account shall mature on the completion of 21 years from the date of the opening of the account. |

| Premature withdrawal | A pre-mature amount of up to 50% of the account balance of the preceding year is allowed for withdrawal for education/ marriage after the account holder turns 18 years or has passed 10th standard whichever is earlier. |

| Premature closure* | Allowed after 5 years only in exceptional circumstances like in the event of death of the depositor or in cases of extreme compassionate grounds such as medical support in life-threatening diseases. In any other case of premature withdrawal, the entire deposit will receive the interest at the rate applicable for the savings bank account. |

| Revival of account | The account can be revived by payment of a penalty of Rs.50 per year, along with the minimum specified amount per year. |

| The maximum number of accounts allowed | One account per girl child subject to a maximum of two accounts per family. (Exception: 3 accounts if the birth was given to twin girl child/ triplet girl child) |

| Can an NRI open an SSY account? | An NRI cannot open an SSY account till they are residing outside India. But once they return to India, they can open an account in the name of a girl child. |

Advantages of opening an SSY account:

-

- Competitive Interest rate.

- Tax benefit available under Sec 80C of Income Tax act.

- Interest earned is tax-free.

- Maturity amount is exempted from tax.

- Maturity amount to be given directly to the girl child.

- The account can be transferred anywhere in India.

- Girl child/Account holder may operate her account if she wishes to. This would give a lot of financial independence to the girl child as well once she becomes a major.

- There is no restriction on the number of times a deposit is made in the account. The depositor can deposit in multiple of Rs. 50 throughout the year.

Shortcomings or Drawbacks:

-

- The lock-in period is slightly on a higher side.

- The account is limited to two girl child of the parents.

- The government resets the interest rate every quarter. Hence the interest rate is not fixed.

The scheme is beneficial for people who are looking for a safe investment option with an attractive tax-free return. However, before making any investment decision, it is wise to compare the scheme with other investment options available in the market.

Comparative Analysis with other Tax saving schemes:

Tax saving FD is one comparable investment. Interest earned under this option range from 5.5% to 7.5%. The lock-in period in these FDs is 5 years (lower than the SSY scheme). Though investment in this FD allows you to claim deduction u/s 80C, the interest earned is taxable. Hence, your net return is not very lucrative.

PPF is another option available that is comparable to the SSY as it also falls under the EEE basket which means that the interest earned is tax-free, and the amount received on maturity is tax-free. Further, the amount invested under this scheme is eligible for deduction u/s 80C. The current interest rate offered under this scheme is 7.1%, which is lower than the SSY scheme.

However, one can’t ignore the fact that PPF allows you to avail loan on the amount invested between the 3rd and 5th year. Also, partial withdrawal is allowed under this scheme on completion of 6 years. This facility is not available under SSY.

Equity Linked Savings Scheme (ELSS) is also a comparable option wherein you invest in the stock market. ELSS offers the possibility of higher returns, but these are not guaranteed as it is linked to the performance of the stock market. ELSS has a lock-in period of 3 years and investment under this scheme is eligible for deduction u/s 80C. The returns are partially taxable though. If you understand the stock market, ELSS is a good investment option.

Investment decision varies for everyone based on income level, existing liabilities, future goal, and risk appetite. The target is to create a healthy corpus for future needs by minimizing the risk and maximizing the returns. Hence, a good way of investment would be to diversify your investment portfolio over a range of available products after proper evaluation.

9 thoughts on “Sukanya Samriddhi Yojana (SSY)”

Leave a Reply

Related Posts

Equity Linked Savings Scheme (ELSS)

Trading Account v/s Demat Account

Very much needed information…Thanx

Thank you

Great info

Thank you.

Very Helpful

Thank you

Very helpful info.

Thank you so much!